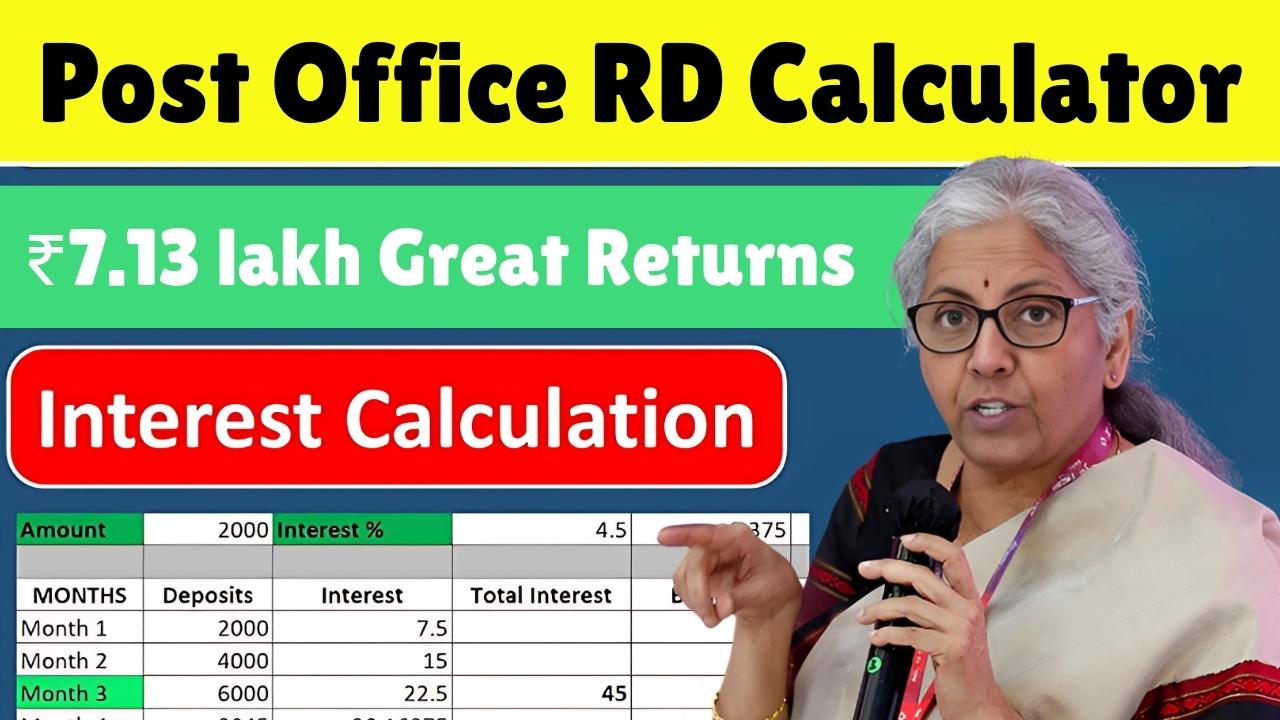

Post Office RD Calculator 2025: ₹10,000 Monthly Deposit Maturity Value Revealed

The Post Office Recurring Deposit (RD) scheme is one of the most trusted small savings products in India. Backed by the Government of India, it ensures complete safety of your money while giving assured returns. This scheme is perfect for individuals who want to save a fixed amount every month and gradually build a sizeable corpus with the help of compound interest.

Although the usual tenure is five years, here we will focus on a three-year investment horizon and how it can benefit investors in 2025.

How the Plan Works

If you decide to invest ₹10,000 every month in a Post Office RD from 2025, your total contribution in three years will be ₹3.6 lakh. At the prevailing interest rate of about 6.7% per annum compounded quarterly, your maturity value will be approximately ₹7.13 lakh. This almost doubles your invested amount within 36 months while keeping your capital safe from market risks.

The scheme is particularly useful for people who prefer stable returns and want to avoid the uncertainty of equity or mutual funds. It can also serve as a reliable option for funding medium-term goals like higher education, buying a vehicle, or building an emergency fund.

The Power of Compounding

The reason Post Office RD delivers attractive results lies in the compounding of interest every quarter. Each time the interest is added, it becomes part of the principal, and the next round of calculations is done on this larger base. As the cycle continues, the growth accelerates even though your monthly deposit remains constant.

This compounding effect makes disciplined saving highly rewarding, turning consistent deposits into a significant lump sum.

Who Should Invest in Post Office RD?

- Salaried individuals who prefer safe, systematic saving

- Retirees and senior citizens who want assured growth without risk

- Parents saving for children’s short-term education goals

- Young professionals building an emergency or contingency fund

The scheme is designed for conservative investors who value predictability and government assurance.

Tax Considerations

Interest earned from a Post Office RD is taxable as per your income slab. There is no Section 80C benefit for deposits, unlike some other schemes such as PPF or NSC. The Post Office does not deduct TDS on RD interest, but you must declare the income while filing tax returns.

This means while the returns are guaranteed, investors should factor in the tax liability before estimating net gains.

How to Open a Post Office RD Account

You can start a Post Office RD account either by visiting your nearest India Post branch or through the online portal (if you already hold a Post Office savings account with internet banking). The account can be opened individually, jointly, or in the name of a minor.

Documents like Aadhaar, PAN, and address proof are required. Once the account is set up, you can deposit manually every month or set up automatic payments. Missing more than four installments could lead to account discontinuation, so automation is often the safest option.

Why Choose Post Office RD Over Other Schemes?

- Government-backed, making it virtually risk-free

- Higher interest rates compared to many bank RDs

- Disciplined savings through fixed monthly contributions

- Accessible even to small savers who cannot invest lump sums

For investors looking for balance between safety and decent returns, this scheme often outperforms bank deposits in terms of reliability and interest earned.

Key Highlights of Post Office RD 2025

| Feature | Details |

|---|---|

| Tenure | 3 years (customized) |

| Monthly Deposit | ₹10,000 |

| Total Contribution | ₹3,60,000 |

| Current Interest Rate | 6.7% p.a. (compounded quarterly) |

| Maturity Amount | Approx. ₹7,13,000 |

| Risk Factor | Virtually nil (Government-backed) |

| TDS Deduction | Not applicable |

| Taxation | Fully taxable as per slab |

| Premature Closure | Allowed after 3 years under conditions |

Conclusion

Investing ₹10,000 every month in a Post Office RD for three years can help you build a maturity corpus of around ₹7.13 lakh. The combination of guaranteed returns, government security, and the effect of compounding makes it an excellent choice for those aiming at short- to medium-term financial goals. While the interest is taxable, the scheme remains one of the safest and most predictable investment avenues for disciplined savers.

Disclaimer

This article is for educational purposes only. Returns are based on current interest rates and are subject to change as per government revisions. Always verify the latest details with the Post Office before investing. Tax implications vary depending on individual circumstances, so consult a financial advisor if necessary.