Financial stability and wealth creation are priorities for every individual, and the Public Provident Fund (PPF) continues to stand out as one of India’s most reliable savings options. Introduced decades ago, this government-backed scheme has remained a top choice for those seeking guaranteed returns, tax benefits, and long-term financial growth.

In 2025, the Post Office PPF continues to maintain its popularity due to attractive interest rates, flexibility in deposits, and assured returns. It blends safety with growth, offering investors a dependable foundation for financial planning and future security.

Understanding the Public Provident Fund

The PPF is a long-term savings scheme initiated by the Government of India to encourage regular saving habits among citizens. It comes with a maturity period of 15 years, which can be extended in blocks of five years. Investors can open a PPF account in any post office or authorized bank branch, making it easily accessible across the country.

Being a government-guaranteed scheme, both the principal and the interest are fully secure. This makes it one of the safest avenues for those who wish to avoid market risks while still earning decent returns.

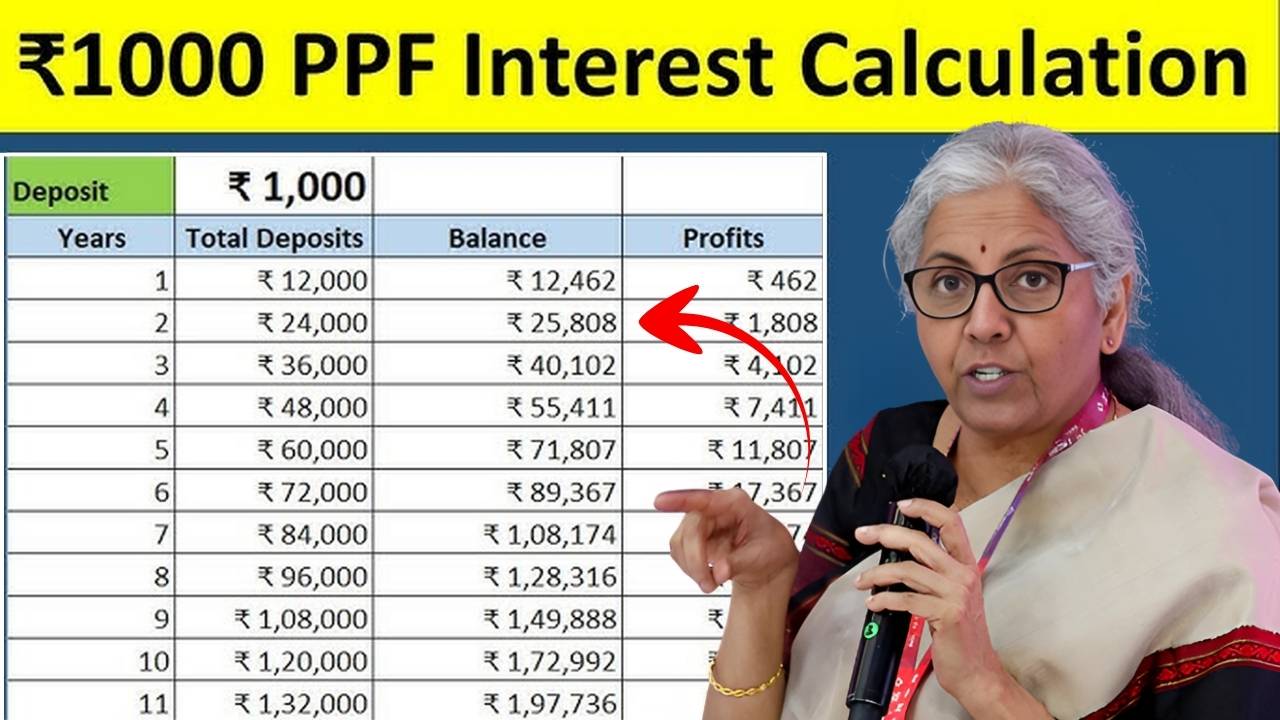

PPF Interest Rate in 2025

The Ministry of Finance revises the PPF interest rate every quarter. In 2025, the rates remain competitive compared to other fixed-return instruments like bank FDs. The interest is compounded annually and credited to the account at the end of each financial year.

Even though the returns are fixed by the government, they are generally aligned with inflation trends, allowing investors to enjoy stable and inflation-adjusted growth.

Tax Advantages of PPF

The Public Provident Fund provides one of the best tax benefits among savings schemes in India. Investments made toward a PPF account qualify for deduction under Section 80C of the Income Tax Act, up to ₹1.5 lakh per financial year.

Additionally, the interest earned and the maturity proceeds are completely exempt from tax, placing PPF in the Exempt-Exempt-Exempt (EEE) category. This makes it highly attractive for those seeking both security and tax-free growth.

Deposit Rules and Limits

The minimum annual contribution required to keep a PPF account active is ₹500, and the maximum allowable deposit per financial year is ₹1.5 lakh. Investors can make deposits either in a lump sum or in up to twelve installments per year.

This flexibility allows individuals to invest as per their financial comfort. It caters to both small savers who prefer regular deposits and high-income earners who wish to maximize tax benefits.

Loan and Withdrawal Options

Though PPF is primarily a long-term savings plan, it offers flexibility for short-term needs. From the third financial year, account holders can avail a loan against their PPF balance at a nominal interest rate. Partial withdrawals are also permitted from the seventh financial year, providing liquidity during emergencies without disturbing the long-term corpus.

Extending the Account After Maturity

Once the initial 15-year period ends, investors can extend their PPF account in blocks of five years. They can choose to extend with or without further contributions. This feature helps investors continue earning tax-free interest while maintaining the security of government backing, making it ideal for long-term wealth creation.

Major Benefits of PPF in 2025

The Public Provident Fund continues to provide several benefits in 2025:

- Safe and government-backed investment option

- Higher interest rates than most fixed deposits

- Full tax exemption on deposits, interest, and maturity amount

- Easy deposit flexibility for all income groups

- Facility for loans and partial withdrawals

- Long-term compounding advantage for wealth creation

These combined features make PPF a stable and practical financial tool suitable for every income segment.

Who Should Invest in PPF

The scheme is well-suited for salaried individuals, self-employed professionals, parents planning for their children’s future, and retirees seeking safe and tax-free income. It is particularly beneficial for those who prefer steady, guaranteed growth rather than high-risk market-based investments.

PPF 2025 Quick Facts and Features

| Feature | Details |

|---|---|

| Scheme Type | Government-Backed Long-Term Savings |

| Maturity Period | 15 Years (Extendable in 5-Year Blocks) |

| Minimum Deposit | ₹500 Per Year |

| Maximum Deposit | ₹1.5 Lakh Per Year |

| Interest Rate (2025) | Announced Quarterly by Ministry of Finance |

| Tax Benefits | Under Section 80C, up to ₹1.5 Lakh |

| Interest & Maturity | Fully Tax-Free (EEE Category) |

| Loan Availability | From 3rd Financial Year |

| Partial Withdrawals | From 7th Financial Year |

| Extension Option | After 15 Years, in 5-Year Blocks |

Conclusion

The Post Office Public Provident Fund remains one of the most dependable and rewarding investment options in 2025. It offers a unique blend of safety, steady returns, tax efficiency, and long-term flexibility. For individuals planning their retirement, children’s education, or future wealth creation, PPF continues to be a preferred choice.

By investing regularly and taking advantage of compounding, investors can build a secure and sizeable corpus over time. With the government’s assurance and steady returns, the PPF stands as one of the most trusted instruments in India’s financial landscape.