Owning a personal vehicle today isn’t about luxury it’s about convenience and independence. Whether you choose a car or a bike, most buyers rely on loans to make the purchase smoother. But a common question arises: is a car loan really better than a bike loan? While both are easy to get from banks and NBFCs, differences in EMI, interest rate, and income eligibility can make one option more suitable than the other.

Understanding the Interest Rate Gap

In 2025, car loan interest rates generally range from 8.5% to 10.5%, based on your credit score and the bank’s lending policy. Bike loans, on the other hand, tend to be slightly higher usually between 10% and 12.5%. The reason is straightforward: cars involve higher loan amounts, which makes them less risky for lenders. Bike loans are smaller and shorter in tenure, so lenders charge a bit more interest to balance the risk.

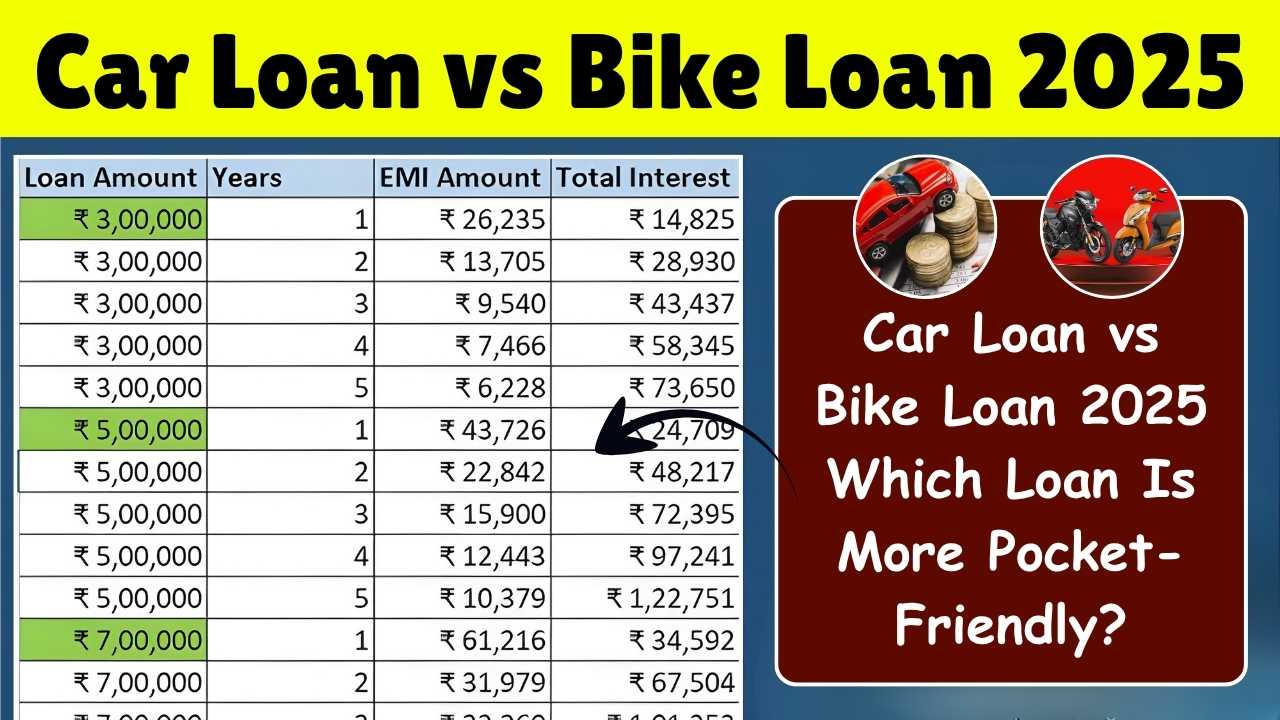

EMI Comparison: Car Loan vs Bike Loan

Let’s understand this with a simple example. Suppose you take a ₹5,00,000 loan for a car and a ₹1,00,000 loan for a bike, both for a period of 5 years.

EMI Comparison Table

| Loan Type | Loan Amount | Interest Rate | Tenure | EMI (Approx) | Total Interest | Total Payment |

|---|---|---|---|---|---|---|

| Car Loan | ₹5,00,000 | 9% | 5 Years | ₹10,378 | ₹2,22,680 | ₹7,22,680 |

| Bike Loan | ₹1,00,000 | 11% | 5 Years | ₹2,174 | ₹30,440 | ₹1,30,440 |

From this table, it’s clear that while the car loan involves a larger monthly outflow, the overall cost as a percentage of the borrowed amount is lower. Bike loans are easier on the monthly budget but relatively expensive when you compare the interest cost to the principal.

Salary and Eligibility Criteria

Before approving any loan, banks carefully evaluate the applicant’s income. Typically, a minimum monthly salary of ₹20,000 to ₹25,000 is required for a car loan. For bike loans, eligibility is more relaxed many lenders approve applications even with ₹10,000 to ₹12,000 income, especially in smaller towns or through NBFCs. This makes bike loans more accessible for those with limited earnings.

Which Loan Offers Better Value?

In simple terms, car loans provide better value if you can handle higher EMIs. The interest rates are lower, and the repayment terms are often more flexible. Bike loans, however, remain the preferred choice for people who need quick mobility without stretching their finances too thin. They’re easier to obtain and manageable for those with modest incomes.

Conclusion

Car loans are generally more cost-effective in the long run due to lower interest rates, while bike loans offer easier accessibility with smaller EMIs and lower income requirements. A ₹5 lakh car loan may demand higher payments each month, but it’s cheaper in total interest percentage. Meanwhile, a ₹1 lakh bike loan suits those looking for an affordable short-term solution. Your decision should ultimately depend on your financial comfort, purpose, and repayment capacity.

Disclaimer

This article is intended for informational purposes only. Loan terms, interest rates, and eligibility conditions vary across financial institutions and may change over time. Always confirm the latest details with your bank or NBFC before applying.