As financial uncertainty continues to shape investment choices, post office saving schemes remain one of the most trusted avenues for Indian investors. These plans, supported by the Government of India, provide safety, predictable returns, and in some cases, tax advantages. For individuals who prioritize stability over market-linked risks, 2025 once again highlights the importance of these savings options.

Understanding Post Office Saving Schemes

Post office saving schemes are designed to encourage disciplined savings and are managed under the Ministry of Finance. Popular across rural, semi-urban, and urban regions, these schemes come with sovereign backing, making them nearly risk-free. Interest rates are reviewed every quarter, but once you invest, the applicable rate is usually fixed for the tenure of your deposit.

Different schemes are tailored for varied needs whether for monthly income, long-term wealth accumulation, or education planning. This wide variety makes them suitable for all types of savers.

Latest Interest Rates (April–June 2025)

For the second quarter of 2025, the government has announced updated rates for small savings instruments.

- Post Office Savings Account: 4% per annum

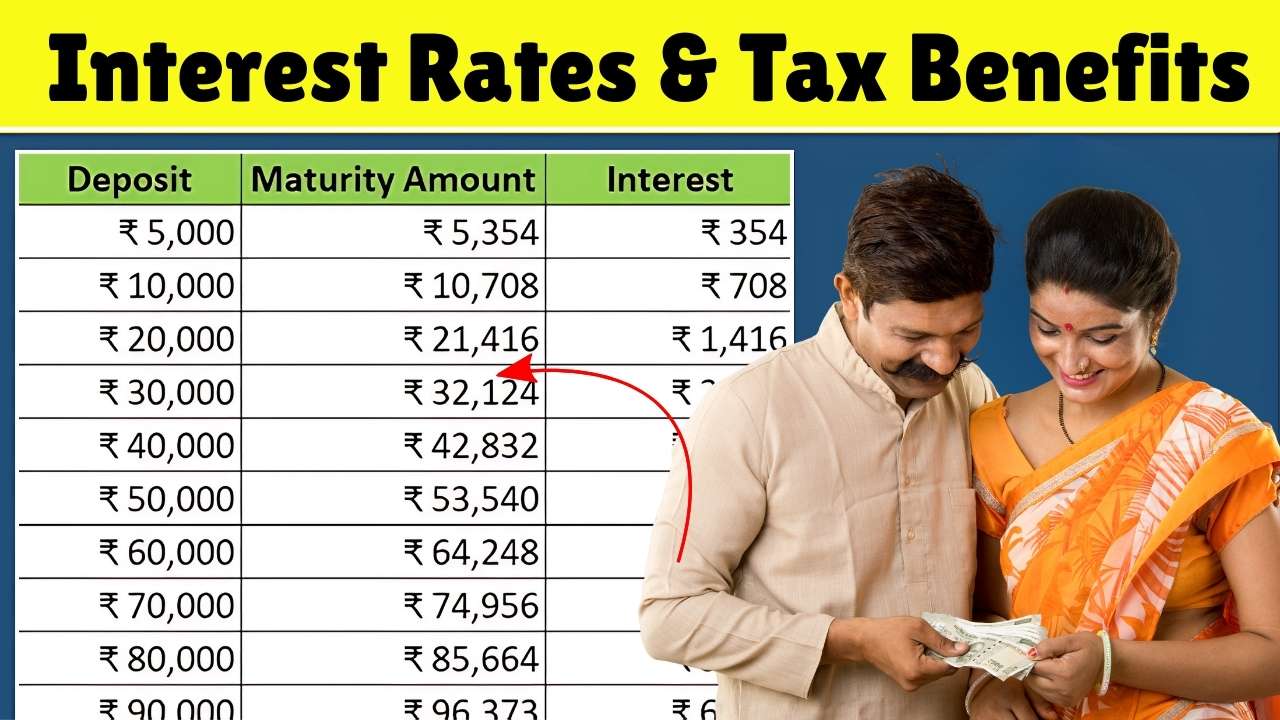

- Time Deposits: 6.9% (1-year), 7.0% (2-year), 7.1% (3-year), 7.5% (5-year)

- Recurring Deposit (5 years): 6.7%

- Monthly Income Scheme: 7.4%

- National Savings Certificate (NSC): 7.7% (compounded annually, payable at maturity)

- Public Provident Fund (PPF): 7.1%

- Sukanya Samriddhi Yojana: 8.2%

- Kisan Vikas Patra: 7.5% (maturity in 115 months)

- Senior Citizens’ Savings Scheme: 8.2% with quarterly payouts

These figures are valid from April to June 2025, though future adjustments will depend on inflation trends and government policies.

Tax Benefits in 2025

Several post office schemes qualify for tax deductions under Section 80C of the Income Tax Act, including PPF, NSC, Sukanya Samriddhi Yojana, the 5-year fixed deposit, and the Senior Citizens’ Savings Scheme.

Interest treatment differs across schemes. PPF and Sukanya Samriddhi are fully tax-free, while NSC interest is taxable but reinvested each year (and thus eligible for deduction except in the final year). Senior Citizens’ Savings Scheme interest is taxable and may attract TDS if thresholds are crossed.

Time deposits, recurring deposits, and the Monthly Income Scheme generate taxable interest, though their predictable nature makes them valuable for conservative investors despite post-tax reductions.

Matching Schemes to Your Goals

- For retirement planning: PPF and Senior Citizens’ Savings Scheme

- For children’s education or future: Sukanya Samriddhi Yojana

- For medium-term goals: NSC and Kisan Vikas Patra

- For regular payouts: Monthly Income Scheme or SCSS

- For short to medium-term savings: Time deposits and recurring deposits

These schemes allow investors to align their financial planning with their goals, balancing safety with stable growth.

Safety, Accessibility, and Ease

A key strength of post office schemes is accessibility. With over 1.5 lakh branches nationwide, even in remote villages, they remain easy to open and maintain. Most schemes allow nomination and premature closure under specific conditions, offering flexibility. While their returns are modest compared to equities or mutual funds, the assurance of government backing provides unmatched peace of mind.

Interest Rates and Tax Benefits at a Glance

| Scheme | Interest Rate (Apr–Jun 2025) | Tax Benefits | Notes |

|---|---|---|---|

| Savings Account | 4% | No | Basic savings option |

| 1–5 Year Time Deposits | 6.9%–7.5% | 5-year qualifies for 80C | Fixed tenure, secure |

| 5-Year RD | 6.7% | No | Disciplined monthly savings |

| Monthly Income Scheme | 7.4% | No | Regular monthly payouts |

| NSC | 7.7% | 80C | Interest taxable but reinvested |

| PPF | 7.1% | 80C + tax-free interest | 15-year lock-in |

| Sukanya Samriddhi Yojana | 8.2% | 80C + tax-free | For girl child |

| Kisan Vikas Patra | 7.5% | No | Matures in 115 months |

| Senior Citizens’ Savings Scheme | 8.2% | 80C | Quarterly payouts, taxable interest |

Final Thoughts

Post office saving schemes in 2025 continue to provide a safe mix of consistent returns, government backing, and tax efficiency. They remain an excellent choice for conservative investors and families seeking long-term financial security. While these schemes may not suit those chasing high-risk, high-reward opportunities, their simplicity and reliability make them a cornerstone of stable financial planning.

Disclaimer: This content is for informational purposes only and should not be taken as financial advice. Interest rates and tax rules may change. Please check official updates or consult a financial advisor before investing.